When you are seeking what is resident status in Malaysia, it is important to know the answer in order to know the tax liability, tax rates, and whether you qualify to get personal reliefs. Tax residency has a direct impact in the determination of your income in Malaysia taxation under the Income Tax Act 1967 and implemented by the Inland Revenue Board of Malaysia (LHDN).

Being an employee, expatriate, director, or business owner, understanding your residency classification is something that will keep you on the correct path of compliance and avoid tax mistakes that can cost you dearly.

To address the clear question of what is resident status in Malaysia clearly, we need to refer to the income tax law.

In Malaysia, the residency status is only measured against the tax status assigned to a particular person in a given year of assessment. It is not determined by:

Rather, it is based solely on the fact that you must be in Malaysia during a calendar year.

Every year, a person is categorized as either:

This classification defines:

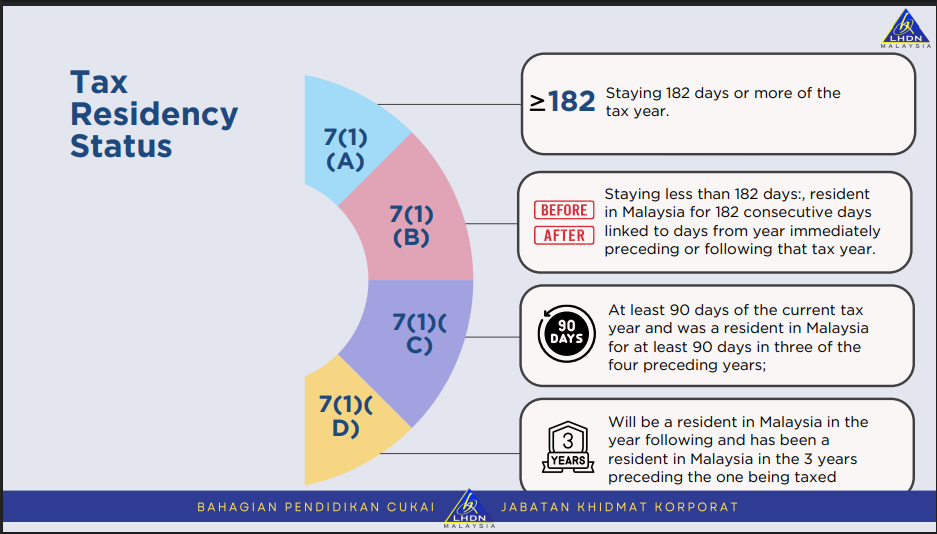

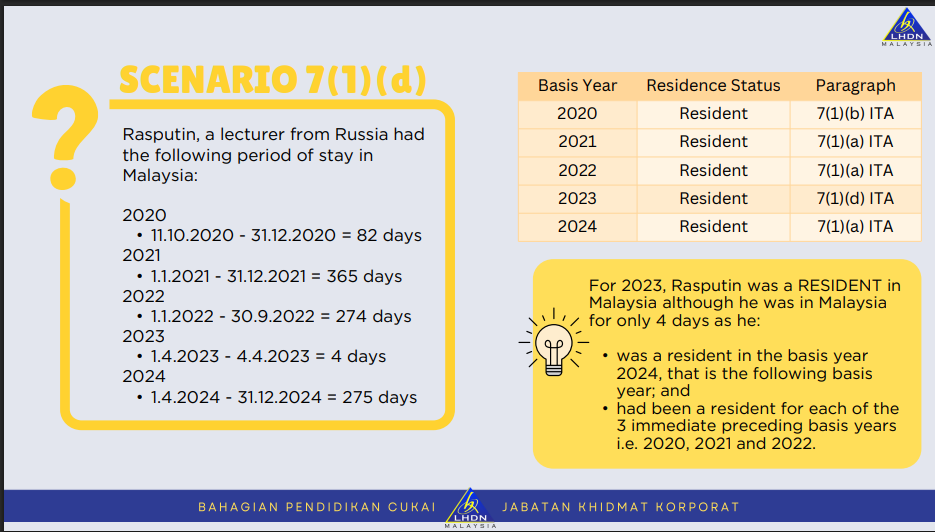

The determination of tax residence falls under the provision of Section 7 of the Income Tax Act 1967. The law presents four statutory tests that are applied in assessing whether one is a Malaysian tax resident or not.

These are the statutory tests which should be used with prudence to ascertain residency.

These rules are important to understand in the case of assessing what is resident status in Malaysia in your situation.

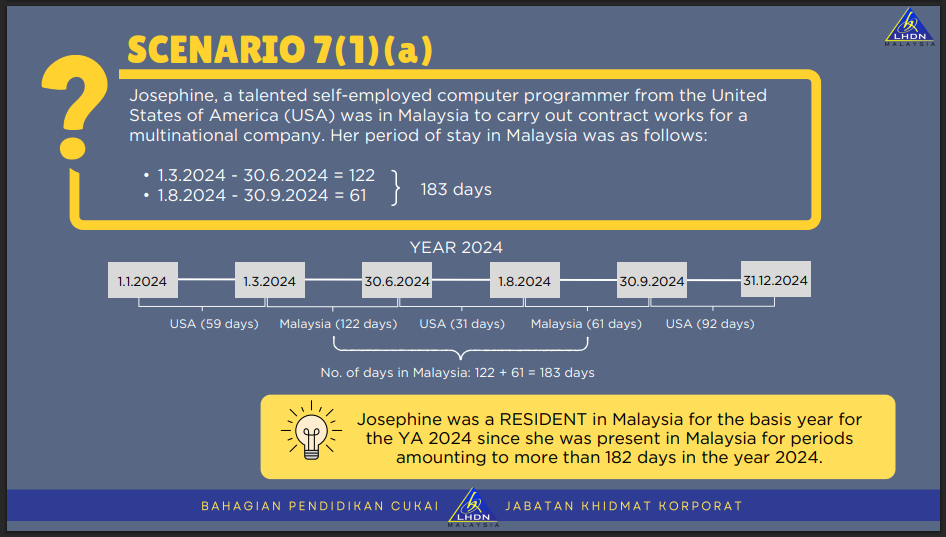

The tax resident status is applied to determine an individual as a tax resident when a tax resident spends 182 days in Malaysia or more in a year of the calendar year.

Important technical points:

It is the most widespread test that is used on employees and expatriates.

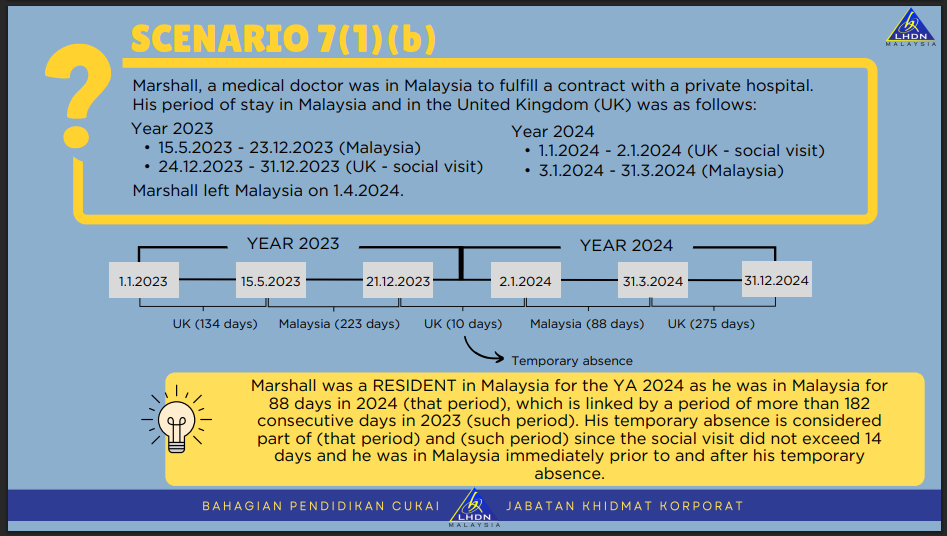

You can also be considered a resident provided:

This is usually applicable in case of a cross-tax year employment.

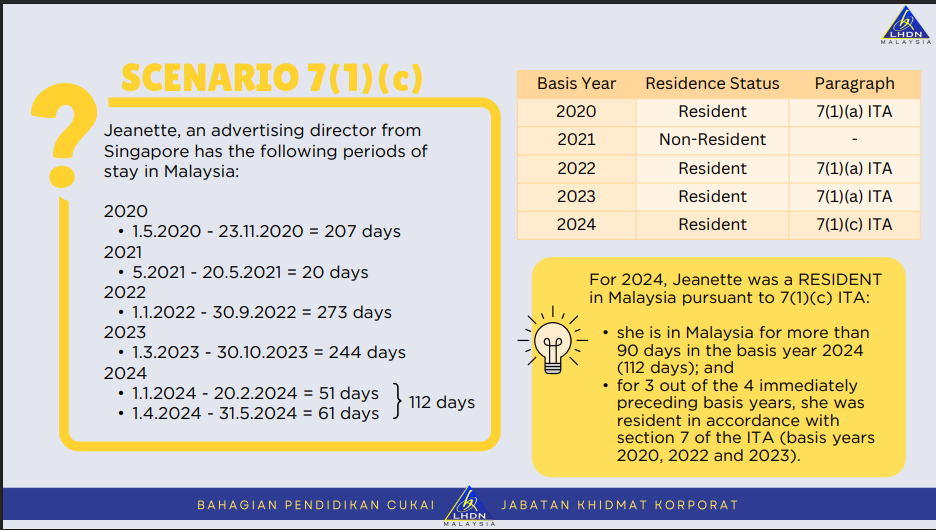

You qualify as a resident if:

This secures continuity among long time taxpayers.

You can also be considered as resident of the current year as follows:

This ensures that temporary short stay does not deprive established taxpayers of resident benefits.

The most significant difference when it comes to analyzing what is resident status in Malaysia is the issue of tax rates.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For income tax purposes:

One of the primary factors that define the liability of an individual to the Malaysian income tax is the residence status.

The liability of taxes is calculated annually.

You may not be taxable if:

Provided that you are a taxable taxpayer that is not a resident, you must submit the M Form to LHDN.

Some temporary leaves can be discussed during your qualifying period in case it is connected with:

Residency claims need to be supported by proper documentation.

To ascertain the status of residence, employers need to establish the status of the employee to:

Misclassification can expose the employer and the employee to audit risks.

Accuracy is essential to avoid needless exposure to taxation.

The definition of resident status in Malaysia is not only technical in nature, but it has direct effect:

Since the residency is determined after a year, both individuals and employers should be closely monitored to ensure physical presence.

At HL Khoo Group, we provide tax planning services for individuals and companies, so you can focus on growing your business while we handle your tax matters.

Resident status is based entirely on physical presence days in Malaysia under Section 7 of the Income Tax Act 1967.

Not always. You may qualify under alternative tests such as the linked consecutive period rule or the 90-day rule with prior residency.

Non-residents are taxed at a flat 30% rate and are not eligible for personal reliefs.

No. Visa type does not determine tax residency. Only physical presence days are relevant.

Vietnam

Vietnam