Sales and Service Tax (SST) in Malaysia is an important element in the tax system of the country. In 2018, SST, which replaced the Goods and Services Tax (GST), is expected to ease the burden on the consumer and to make goods and services more cost-effective. By 2025, SST will remain the basis of indirect taxation in Malaysia. This detailed guide review outlines all the key information about SST: what it is, how it is structured, what are the rates, how to comply with it, and the effects on businesses. Its recent developments on the changes that will be made to sales tax rates as of 1 July 2025 have been also stated.

Overview of SST in Malaysia

The Sales and Service Tax (SST) is divided into two different components:

Sales Tax: the tax levied at the manufacturing and importation of goods level of what is manufactured and imported.

Service Tax: It is charged on the payment of some of the specified services given by the taxable persons in Malaysia.

The two taxes are issued under different legislations:

Acts 2018 No 13 Sales Tax Act

Service Tax Act 2018

The Royal Malaysian Customs Department (RMCD) is the body with powers to administer SST.

Sales Tax: Scope, Rates, and Applicability

What Sales Tax is?

Sales Tax in Malaysia is directly imposed on a taxable commodity which is either produced or imported to the country. It is not paid at all points during the supply chain but only when it is manufactured or imported.

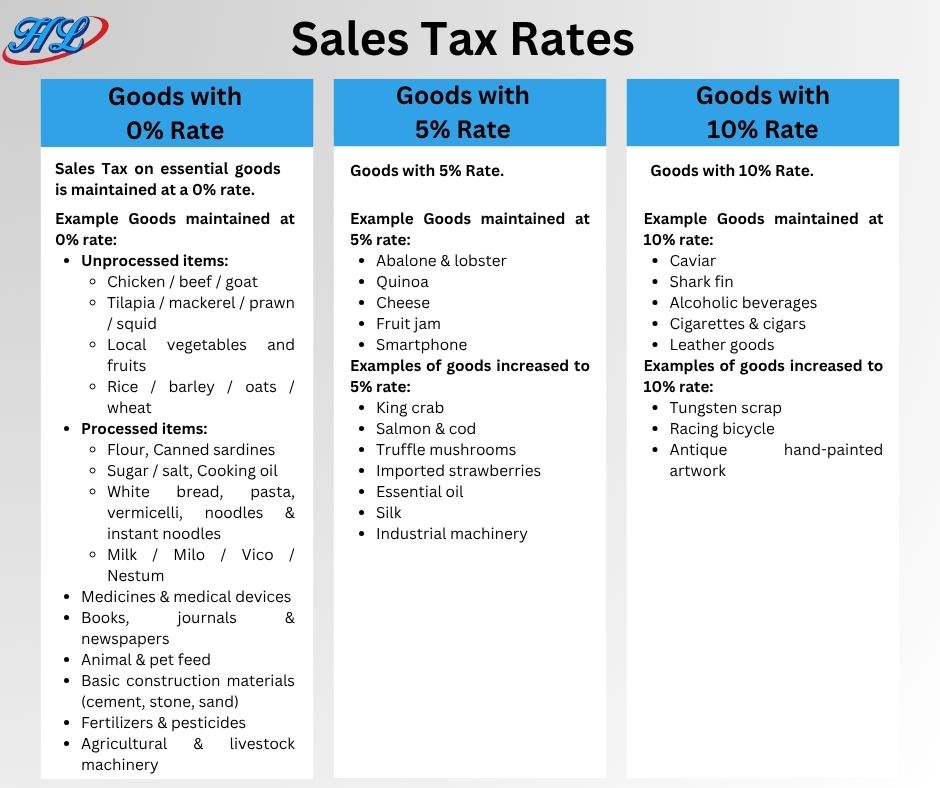

Sales Tax Rates (Updated 2025)

On 1 July 2025, Malaysia changed its Sales Tax rates:

5%- It is charged on necessities and less valuable commodities

10% Which is imposed on the majority of the standard manufactured goods

Specific rate RM per unit on items of choice (e.g. beverages, petroleum)

Tax rate is imposed based on the date of issuance of the invoice or date of customs clearance where the date on which the product is produced or bought does not determine the tax rate.

Examples:

Invoice created before 1 July 2025- old rate will be applied

An invoice that was issued on/after 1 July 2025- needs to be dealt with under the new rate

Taxable Goods

Items subject to sales tax are:

Locally produced goods excluding the exemptions

Any imported goods unless given an exemption in the Sales Tax (Goods Exempted from Tax) Order 2025

Basic foodstuffs, medical equipment and reading materials are usually not taxed.

Own Use or Disposal of Manufactured Goods

Even where the registered manufacturers consume or discard goods within themselves, they must charge SST e.g. :

Promotional giveaways

Consumption or in house testing

CSR/ free sampling

Where the use/disposal is on or after 1 July 2025, the new tax rate is applicable despite the time at which the company had incurred the same in its books of account.

Example:

Goods registered with own use 25 May 2025

Physical consumption on 15 July 2025 10% tax will be applicable (Ref: Situation 7, Customs Guideline)

Sales Tax Exemption for Manufacturers

Effective 1 January 2026

Registered manufacturers are exempted from Sales Tax on critical raw materials, including: • Fertilisers • Animal feed • Pesticides

This measure helps stabilise the prices of essential goods.

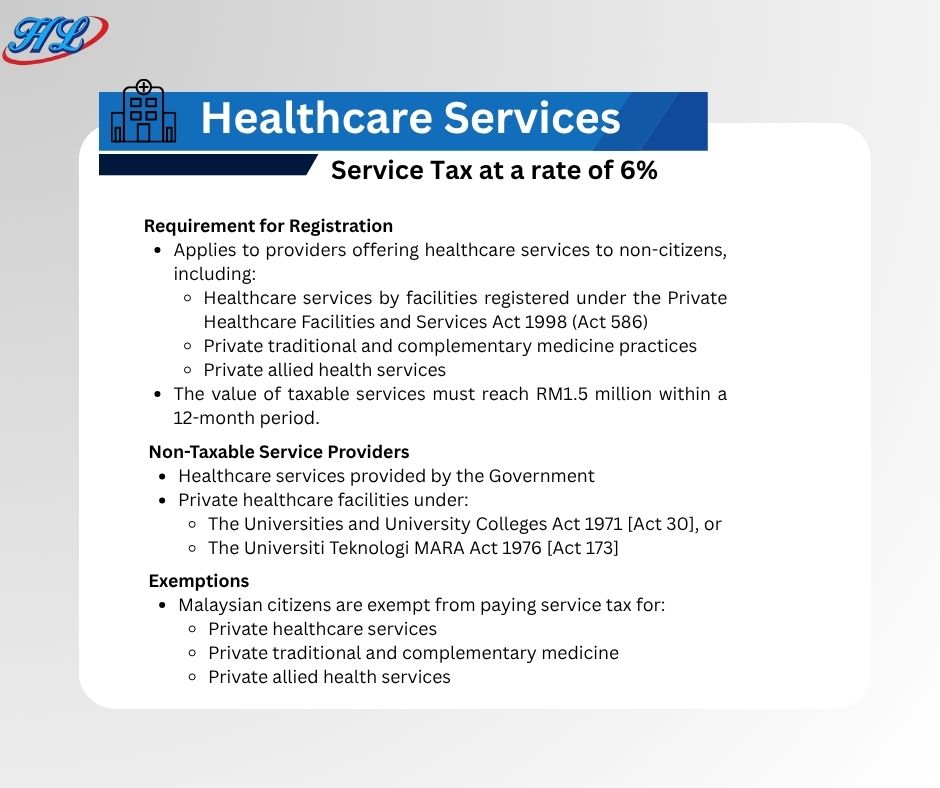

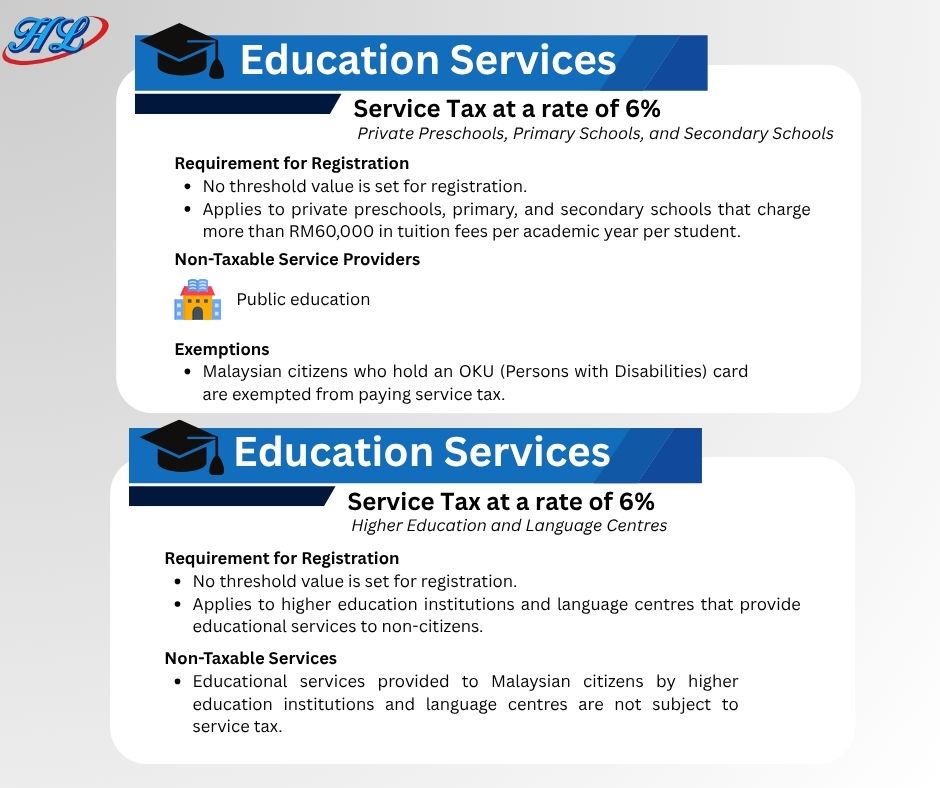

Service Tax- Scope, Rates and Applicability

What Is The Service Tax?

Service Tax is charged on the taxable services provided in Malaysia by a registered person. It is an end consumption tax.

Service Tax Rate (2025)

As of 2025, the normal Service Tax charge will be 6%, but there will be further expansion of scope:

Logistic services and courier services have become taxable now

Foreign online service providers (e.g. Netflix, Spotify) have to be registered

Taxable Services

Some worth mentioning lines of taxable services are:

Hotel, accommodation

F&B (cafes, restaurants)

Professional service (lawyers, accountants)

Telecommunications (internet, mobile services)

Insurance Takaful

Streaming and online services

Updated Service Tax Rates (2025)

Exempted Services

Public Transportation Services

Public transportation remains fully exempt from service tax. This includes:

Vietnam

Vietnam